中国金属行业金融支持效率测算

作者简介: 邵留国,男,山东汶上人,博士,副教授,研究方向为资源经济与管理。E-mail:shaoliuguo@qq.com

收稿日期: 2017-08-15

要求修回日期: 2018-02-05

网络出版日期: 2018-03-10

基金资助

国家自然科学基金重点项目(71633006)

中国博士后科学基金(2017T100124,2016M600162)

湖南省社科基金(16YBA372)

The financial support efficiency of the metal industry in China

Received date: 2017-08-15

Request revised date: 2018-02-05

Online published: 2018-03-10

Copyright

基于Meta-frontier DEA方法测算中国金属上市公司2011—2016年的金融支持效率,并比较各种机制的效率损失强度,包括内部治理、行业环境和所有制。研究结果表明:① 中国金属行业虽然景气不佳,但最主要的制约因素还是内部治理,尽管行业和所有制不同,提高金融支持效率的重心仍然是改善内部治理效率;② 行业环境和所有制的重要性也是不可忽视的,行业效率和所有制效率的改善对金融支持效率有正向作用;③ 相比民企,国企受内部治理、行业环境和所有制效率损失的制约程度都要更大,这意味着国企存在更严重的委托代理、市场依赖性等问题;④ 内部治理效率的行业差异会因行业联系的增强而弱化,这表明降低行业壁垒有益于改善内部治理。

邵留国 , 许铭 . 中国金属行业金融支持效率测算[J]. 资源科学, 2018 , 40(3) : 623 -633 . DOI: 10.18402/resci.2018.03.16

Based on the Meta-frontier DEA method, here we calculated the financial support efficiency and compared various mechanisms for efficiency loss intensity, including internal governance, industry environment and ownership. The losses can be attributed to internal governance, industry environment and ownership factors. These results mainly come from metal-listed companies in China from 2011 to 2016. We found that although the metal industry in China is not prosperous, the most important constraint is internal governance. Even though industry and ownership are different, the focus on improving financial support efficiency is still to improve internal governance. The importance of ownership and industry environments cannot be ignored. The improvement of industry efficiency and ownership efficiency has a positive effect on financial support efficiency. The financial support efficiency will be higher, if industry efficiency and ownership efficiency can be improved. Compared with private enterprise, state-owned enterprises are more constrained in terms of internal governance, industrial environment and ownership. This means that state-owned enterprises have more serious problems such as principal-agent and market dependence. Industry differences in internal governance efficiency will be narrowed because of the enhancement of industry contacts and the knowledge barrier will be smaller as the industry coupling works better. Industry differences in internal governance efficiency will be weakened because of diffusion of knowledge. On the basis of theoretical mechanisms, we build an index system, which gives theoretical and practical value to financial support efficiency.

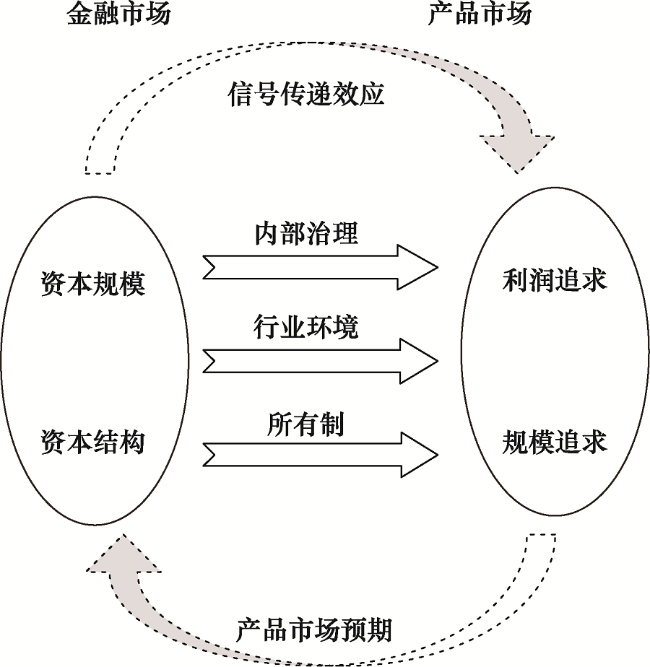

Figure 1 The index selection principle about financial support efficiency图1 金融支持效率指标选取原理 |

Table 1 The mean value of financial support efficiency表1 金融支持效率均值 |

| 钢铁 | 基本金属 | 贵金属 | 合计 | |

|---|---|---|---|---|

| 民企 | 0.63 | 0.60 | 0.68 | 0.62 |

| 国企 | 0.45 | 0.56 | 0.57 | 0.52 |

| 合计 | 0.52 | 0.59 | 0.63 | 0.58 |

Table 2 The KS test results (P value)表2 KS检验结果(P值) |

| 钢铁 | 基本金属 | 贵金属 | |

|---|---|---|---|

| 钢铁 | 1 | 0 | 4e-4 |

| 基本金属 | 1 | 0.028 | |

| 贵金属 | 1 | ||

| 国企与民企KS检验结果 | 0 | ||

注:P值小于e-4记为0。 |

Table 3 The efficiency loss decomposition using Equation (2)表3 应用公式(2)的效率损失分解 |

| 行业 | 所有制 | 内部治理 | ||

|---|---|---|---|---|

| 整体 | 0.06 | 0.04 | 0.33 | |

| 分行业 | 钢铁 | 0.13 | 0.02 | 0.33 |

| 基本金属 | 0.02 | 0.04 | 0.35 | |

| 贵金属 | 0.11 | 0.02 | 0.23 | |

| 分所有制 | 非国有 | 0.05 | 0.03 | 0.30 |

| 国有 | 0.07 | 0.04 | 0.37 | |

Table 4 The KS test about efficiency loss using equation (2)表4 应用公式(2)的效率损失KS检验 |

| 内部治理 | 行业 | 所有制 | ||

|---|---|---|---|---|

| 全部企业 | 内部治理 | 1 | 0 | 0 |

| 行业 | 0 | 1 | 0 | |

| 所有制 | 0 | 0 | 1 | |

| 钢铁行业 | 内部治理 | 1 | 0 | 0 |

| 行业 | 0 | 1 | 0 | |

| 所有制 | 0 | 0 | 1 | |

| 基本金属行业 | 内部治理 | 1 | 0 | 0 |

| 行业 | 0 | 1 | 0 | |

| 所有制 | 0 | 0 | 1 | |

| 贵金属行业 | 内部治理 | 1 | 0 | 0 |

| 行业 | 0 | 1 | 0 | |

| 所有制 | 0 | 0 | 1 | |

| 民企 | 内部治理 | 1 | 0 | 0 |

| 行业 | 0 | 1 | 0 | |

| 所有制 | 0 | 0 | 1 | |

| 国企 | 内部治理 | 1 | 0 | 0 |

| 行业 | 0 | 1 | 0 | |

| 所有制 | 0 | 0 | 1 |

注:P值小于e-4 记为0。 |

Figure 2 Factor significance图2 因素显著性 |

Table 5 The efficiency loss decomposition using Equation (3)表5 应用公式(3)的效率损失分解 |

| 行业 | 所有制 | 内部治理 | ||

|---|---|---|---|---|

| 整体 | 0.05 | 0.05 | 0.33 | |

| 分行业 | 钢铁 | 0.09 | 0.06 | 0.33 |

| 基本金属 | 0.02 | 0.04 | 0.35 | |

| 贵金属 | 0.09 | 0.05 | 0.23 | |

| 分所有制 | 非国有 | 0.04 | 0.04 | 0.30 |

| 国有 | 0.05 | 0.06 | 0.33 | |

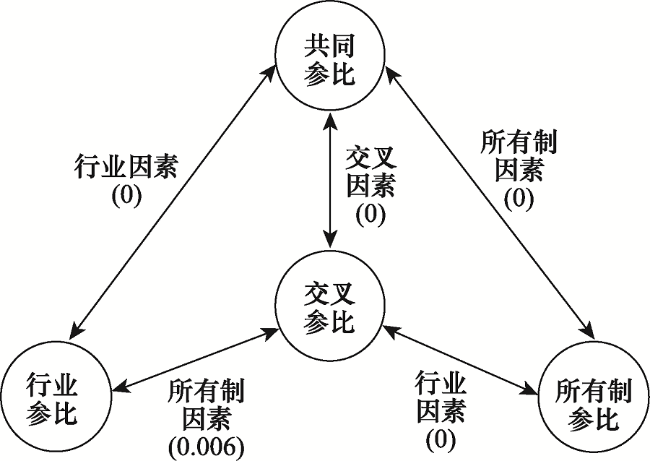

Table 6 The KS test about efficiency loss using equation (3)表6 应用公式(3)的效率损失KS检验 |

| 内部治理 | 行业 | 所有制 | ||

|---|---|---|---|---|

| 全部企业 | 内部治理 | 1 | 0 | 0 |

| 行业 | 0 | 1 | 0.015 | |

| 所有制 | 0 | 0.015 | 1 | |

| 钢铁行业 | 内部治理 | 1 | 0 | 0 |

| 行业 | 0 | 1 | 0 | |

| 所有制 | 0 | 0 | 1 | |

| 基本金属行业 | 内部治理 | 1 | 0 | 0 |

| 行业 | 0 | 1 | 0 | |

| 所有制 | 0 | 0 | 1 | |

| 贵金属行业 | 内部治理 | 1 | 0 | 0 |

| 行业 | 0 | 1 | 0.028 | |

| 所有制 | 0 | 0.028 | 1 | |

| 民企 | 内部治理 | 1 | 0 | 0 |

| 行业 | 0 | 1 | 0.006 | |

| 所有制 | 0 | 0.006 | 1 | |

| 国企 | 内部治理 | 1 | 0 | 0 |

| 行业 | 0 | 1 | 0.008 | |

| 所有制 | 0 | 0.008 | 1 |

注:P值小于e-4 记为0。 |

The authors have declared that no competing interests exist.

| [1] |

|

| [2] |

|

| [3] |

[

|

| [4] |

[

|

| [5] |

工业和信息化部. 有色金属工业发展规划(2016-2020年)[J]. 有色冶金节能, 2016, 32(6):1-10.

[Ministry of Industry and Information Technology. Nonferrous Metals Industry Development Plan (2016-2020)[J]. Energy Saving of Non-ferrous Metallurgy, 2016, 32(6):1-10.]

|

| [6] |

工业和信息化部. 钢铁工业调整升级规划(2016-2020年)[J]. 中国钢铁业, 2016(12):5-13.

[Ministry of Industry and Information Technology. Steel Industry Adjustment and Upgrading Plan (2016-2020)[J] China steel, 2016(12):5-13.]

|

| [7] |

|

| [8] |

|

| [9] |

[

|

| [10] |

[

|

| [11] |

|

| [12] |

[

|

| [13] |

|

| [14] |

|

| [15] |

|

| [16] |

[

|

| [17] |

[

|

| [18] |

[

|

| [19] |

[

|

| [20] |

[

|

| [21] |

[

|

| [22] |

[

|

| [23] |

[

|

| [24] |

|

| [25] |

[

|

| [26] |

[

|

| [27] |

|

| [28] |

|

| [29] |

[

|

| [30] |

[

|

| [31] |

[

|

| [32] |

[

|

| [33] |

[

|

| [34] |

[

|

| [35] |

[

|

| [36] |

|

| [37] |

|

| [38] |

[

|

| [39] |

|

| [40] |

[

|

| [41] |

|

| [42] |

[

|

| [43] |

|

| [44] |

|

| [45] |

[

|

| [46] |

万得资讯. 中国钢铁、基本金属、贵金属上市公司数据 [R]. 上海: 万得金融数据库, 2011-2016.

[Wind Information. Listed Company Data about Steel, Basic Metal and Gold in China[R]. Shanghai: Wind’s financial database, 2011-2016.]

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}